Each year, many of us breathe a collective sigh of relief when April 16 rolls around. Aside from those filing for extensions, and aside from those few who are affected by lesser-known categories, the majority of Americans have completed the filing of their annual income tax returns. And for most, the relief is not just from having fulfilled their federal obligations, but also from having met their obligations under the tax filing requirements of states, cities, and other districts.

Now that the frenzy of “tax season” is over, we can shift gears and look at issues we pushed aside prior to April 15. One of the most frequent questions we at PG Calc receive from our clients is regarding the “tax savings” line on the Summary of Benefits Projection chart. And in order to understand the tax savings concept, we need to understand the charitable income tax deduction. For planned giving professionals, the charitable deduction has always been at the focus of the process, rather like the proverbial pot of gold at the end of the rainbow.

In recent years, however, since the passage of the Tax Cuts and Jobs Act of 2017 (TCJA), there has been somewhat less interest in the charitable deduction. The TCJA dramatically altered the tax-filing patterns of many Americans by almost doubling the standard deduction – which then, logically, became indexed for inflation. In 2025, the standard deduction available for individual taxpayers was $15,750, which translated to $31,500 for a married couple filing joint income tax returns. While data about planned giving donors in particular is hard to find, we know that, for the population as a whole, the percentage of taxpayers filing itemized tax returns has dropped from roughly 30% before the 2017 legislation to roughly 10% since the TCJA legislation.

Many of us believe that the population of planned giving donors skews toward a higher percentage of individuals and couples filing itemized tax returns, based simply on the conversations we have every day. But we think it’s important to review how the itemized deductions really benefit the donors who make use of them. And, in order to do that, we need to talk about one of the least favorite topics in modern-day America: The Form 1040. That is the “standard” federal income tax return with which individuals report their income, deductions, tax payments, and other critically important financial information.

These days, most American taxpayers have become quite unfamiliar with actual tax returns, due to the overwhelming popularity of online tax filing software. We just push some buttons and type in some numbers, and the rest is magic! But the actual tax forms still exist, and we need to look specifically at Form 1040 to see exactly how the numbers work when it comes to charitable deductions. And once we have gotten through that process, we can start to talk about tax savings.

The upper half of the first page of the 2025 Form 1040 is devoted to non-financial information, such as name, address, and filing status. The lower half is all about income. For the most simplified example, we’ll say that the theoretical person is a single individual who earned $100,000 in 2025. If that amount appears in box 1 on the individual’s W-2, it would be entered on line 1a of the Form 1040. We’ll assume that there is no other income to be reported for this individual, so that the “adjusted gross income” (frequently referred to as “AGI”) reported on line 11a is the same $100,000.

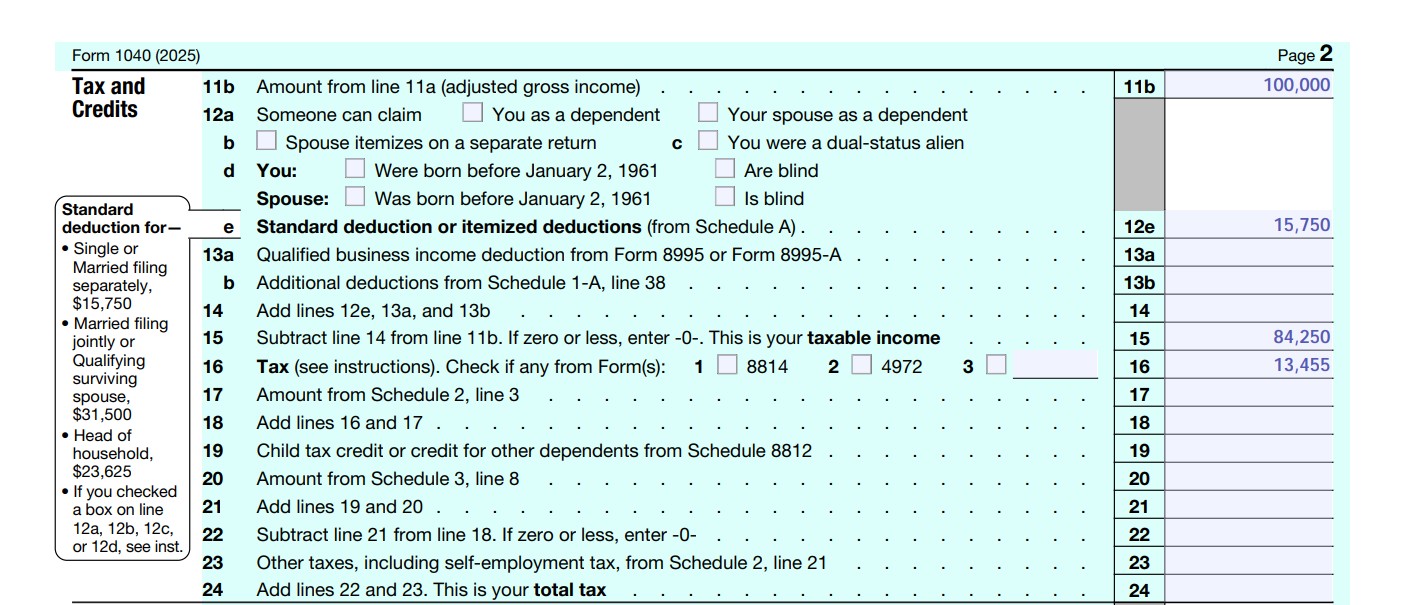

The top part of the second page is about tax amounts and credits. The first line – 11b – is simply repeating the AGI amount of $100,000 from line 11a, the last line of page 1. Then we get into deductions. First, we’ll start with the assumption that the individual is claiming the standard deduction. This amount changes every year, and for 2025, as we mentioned above, the standard deduction is $15,750. That amount is entered on line 12e.

If there are no other deductions, we subtract the $15,750 from $100,000 to get the taxable income of $84,250 which is reported on Line 15. From there, we would go to the tax table for Form 1040 in the IRS Tax Guide 2025 to determine the amount of tax for $84,250 which is $13,455. This is for an overly simplified example of a person who files as a single taxpayer and takes the standard deduction.

To understand the concept of itemized deductions, and to understand the potential reward of taking itemized deductions, we need to look at Form 1040 Schedule A. This form is divided up into Medical and Dental Expenses, Taxes You Paid, Interest You Paid, Gifts to Charity, and a couple of other smaller categories that are not relevant to this discussion.

The first section – Medical and Dental Expenses – is not relevant for many individuals, because those expenses have to exceed 7.5% of the person’s AGI in order to be deductible. We will assume, in this case, that the person did not pay more than $7,500 out of pocket for these expenses.

The second section – Taxes You Paid – is really about state and local taxes. We’ll keep it really simple here and say that the individual paid $5,000 in state income tax and $5,000 in local real estate taxes.

The third section – Interest You Paid – is primarily about the interest paid on home mortgages, within certain parameters. For this individual, we’ll say that the interest paid on the home mortgage was $5,750. There is a specific reason we are using this theoretical amount.

The fourth section – Gifts to Charity (the last relevant section for our discussion) – is for deductions from charitable gifts. Initially, we’re going to assume there are no reportable charitable gifts.

Why are we keeping these numbers so simple? Because the total for our itemized deductions would come to $15,750, and that is exactly the amount of the STANDARD deduction for our theoretical person. Here are three truisms that are very important, so we’re going to put this in a rather dramatic format:

- If the person’s itemized deductions add up to less than $15,750, there is NO NEED to use the itemization option. Using itemized deductions totaling $12,000, for example, would result in MORE income tax than using the standard deduction.

- If the itemized deductions are exactly equal to $15,750, there is also NO NEED to use the itemized deductions approach. The person can simply use the standard deduction and there will be no need to prepare and attach Schedule A.

- It is only if the person’s itemized deductions EXCEED the standard deduction that a person would itemize deductions on a Schedule A. If the total of the itemized deductions is greater than $15,750, then the taxable income will be LESS (compared to using the standard deduction). And if the taxable income is LESS, the amount of income tax will also be LESS.

But now, let’s say the individual is a kind and generous person, and he or she established a charitable gift annuity in 2025. If we add in a charitable tax deduction for the charitable gift annuity (CGA) – that will tip the scales in favor of using the itemized deductions method. Let’s say now that the person established a CGA, and the charitable income tax deduction was calculated to be $10,000 (there is a reason for using that specific amount, explained below). How would that change affect the individual’s tax return and the resulting tax due?

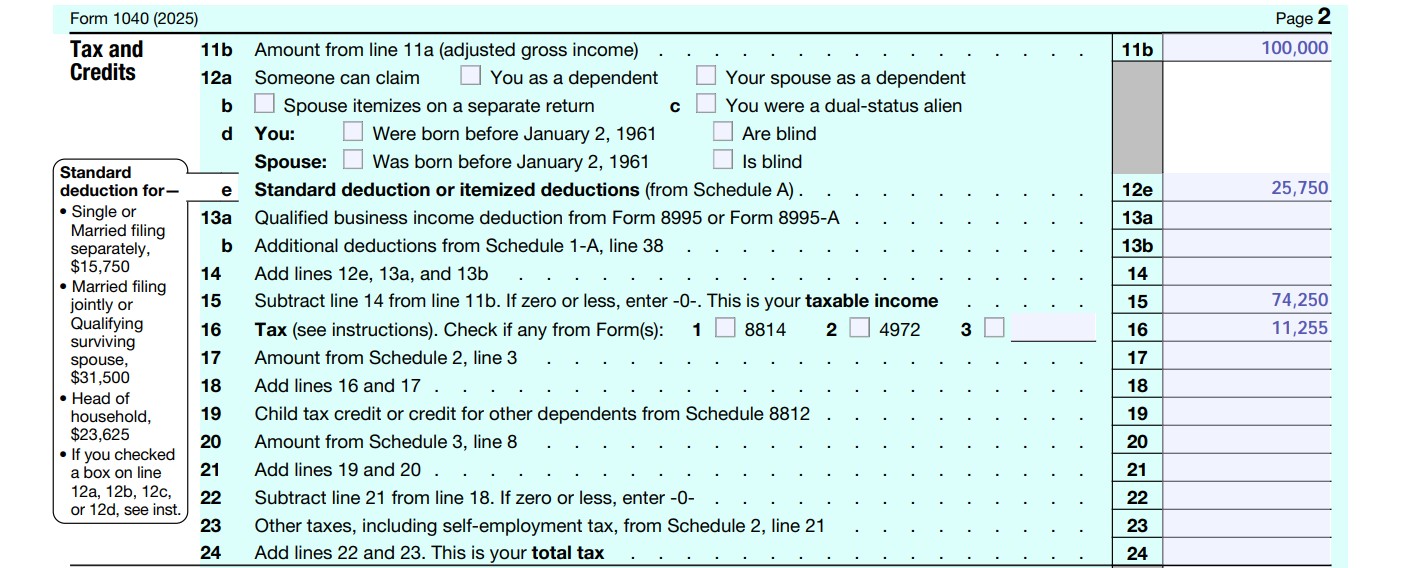

The $10,000 charitable deduction for the gift annuity would boost the total of the itemized deductions from $15,750 up to $25,750. Let’s take a look now at how that would alter the amount of tax due: if the total of itemized deductions were changed to $25,750, that would give us a taxable income of $74,250 ($100,000 income - $25,750 itemized deductions). And the appropriate tax for that amount of income would be $11,255 per the IRS 2025 Tax Table. The difference is significant: the total tax liability goes from $13,455 in the first example to $11,255 in the second example – a difference of $2,200!

This is when we can start talking about tax savings. The donor would save $2,200 from using the $10,000 charitable deduction for the gift annuity. The tax savings in this case would be expressed as 22% ($2,200 ÷ $10,000). The main point is that the amount of the deduction is NEVER the amount of the tax savings. The tax savings are always just a PORTION of the amount of the deduction.

So, how does this look in PG Calc’s PGM Anywhere? We used a gift date of 10/1/2025 for a donor aged 62. We chose a deferred gift annuity, starting payments in 5 years (in 2030), with a payout rate of 7.7%. We used the funding amount of $24,080, so that we would get a charitable income tax deduction of exactly $10,000.

With the charitable deduction at $10,000, on the Summary of Benefits Projection Chart, we get an “income tax savings” amount of $2,200, which is exactly 22% of the deduction amount. This is confirmation that the donor would save $2,200 of actual tax due if he or she claimed the income tax deduction as explained above.

With our examples above, we want to reiterate that the donor saves on the total amount of income tax due by claiming the charitable income tax deduction. Generally speaking, the tax savings will be the amount of the deduction times the income tax bracket, which in this case was 22% (for AGI between $48,475 and $103,350), but it doesn’t always come out exactly that way in real life. If the donor’s other itemized deductions totaled up to less than the magic $15,750, for example, the tax savings on the $10,000 charitable deduction would in fact be less than 22%. It depends on all of the other numbers involved in the situation.

To summarize, here are the main points of this conversation:

- The charitable deduction will only result in tax savings if the total of the donor’s itemized deductions EXCEEDS the amount of the standard deduction. In our example, if the donor did not have any state income tax or property tax, and if the donor didn’t have mortgage interest, the $10,000 charitable deduction by itself would not result in any tax savings.

- The amount of tax savings will ALWAYS be just a PORTION of the total deduction amount.

- The amount of the tax savings will be based on how much of the charitable deduction puts the donor’s total itemized deductions OVER the standard deduction amount.

- Tax savings are always just an ESTIMATE – no planned giving professional will ever know all of the financial details about the specific donor, so the planned giving professional cannot ever be certain of what the tax savings will be.

We hope you find this article helpful. Please feel free to contact us with any questions.