Have Gift Annuity Benefits Peaked for Donors?

-It is no secret that the American Council on Gift Annuities (ACGA) recently increased its suggested maximum annuity rates. The new rates, which went into effect on January 1 of this year, marked the third increase in the ACGA rates in the last 18 months. At typical annuitant ages, the current rates are roughly 1.5% higher than they were in June 2022. For example, the ACGA rate for a 75-year-old annuitant was 5.4% in June 2022 and is 7.0% today.

The larger story is that today’s ACGA rates are the highest they’ve been in 15 years. What does all this mean for gift annuities?

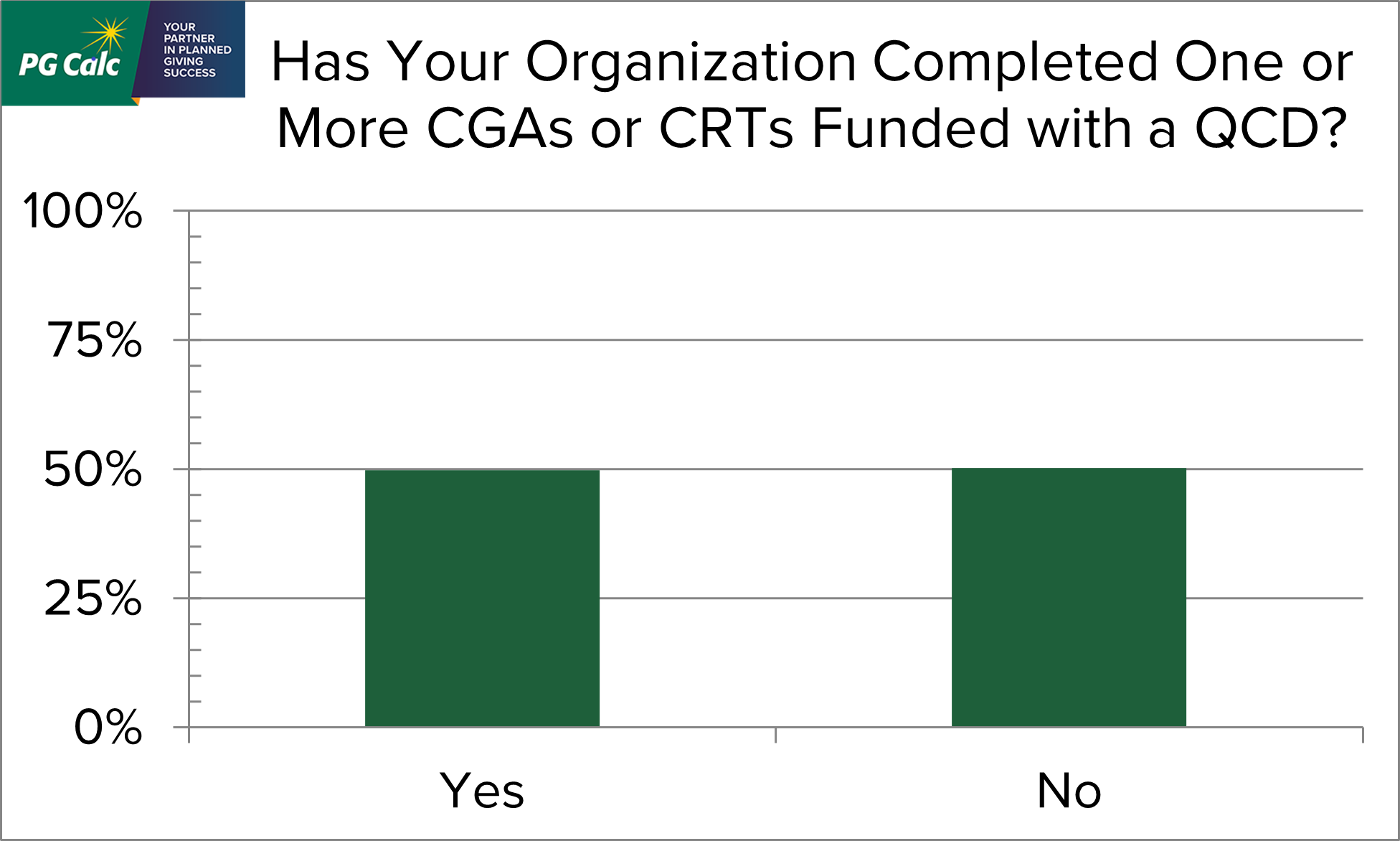

PG Calc QCD Survey: Many Charities Report Closing CGAs Funded With a QCD

-

A new gift planning opportunity became available at the beginning of this year thanks to the Legacy IRA Act that passed late last December: funding a charitable gift annuity (CGA) or charitable remainder trust (CRT) with a qualified charitable distribution (QCD) from one’s IRA. Gift planners were rightfully excited to have a new gift plan to talk about with their donors. However, the new gift plan’s many requirements raised doubts about how popular it would be. Who would make these gifts? Now that we are most of the way through 2023, the QCD for life income plan’s place in planned gift fundraising has become clearer.

A new gift planning opportunity became available at the beginning of this year thanks to the Legacy IRA Act that passed late last December: funding a charitable gift annuity (CGA) or charitable remainder trust (CRT) with a qualified charitable distribution (QCD) from one’s IRA. Gift planners were rightfully excited to have a new gift plan to talk about with their donors. However, the new gift plan’s many requirements raised doubts about how popular it would be. Who would make these gifts? Now that we are most of the way through 2023, the QCD for life income plan’s place in planned gift fundraising has become clearer.

In their interactions with clients, our Client Services and Gift Administration teams have noticed a recent increase in the number of new CGAs funded with a QCD. This pattern piqued our interest. To investigate the popularity of this new gift option further, we sent out a survey to a broad fundraising audience. We summarize our results below.

Measuring the Success of Your CGA Program: The Case for Maintaining Current Market Values for All Charitable Gift Annuities

-Charitable gift annuities (CGAs) are designed to be the split-interest gift for any donor. The basic premise is that the donor contributes cash or marketable securities to a charitable organization, and the charity promises to make payments to the donor for the rest of his or her life. The donor receives a charitable income tax deduction at the time of the gift, and some portion of the original principal remains at the donor’s passing.

That all sounds great, right? A classic “win-win-win” arrangement, and in fact, most charitable gift annuities result in a significant portion of the original principal as the residuum. When a charity has a robust gift annuity program, there can be enormous financial rewards from the ongoing stream of CGA terminations. But we’ve all heard the other side of the story as well. There are far too many examples where the gift corpus becomes completely used up, and in fact, the charity ends up kicking in money from general funds to continue making payments to an annuitant who lived beyond their original life expectancy. We call these “underwater gift annuities,” and they actually end up with negative dollar benefits.

So, what is the sum total benefit of this gift annuity venture from the charity’s perspective? Put simply, how does the charity even begin to measure the success of their CGA program?

Funding CGAs with Mutual Funds – Is This Still a Problem?

-Americans have extensive holdings of mutual funds representing significant portions of their investment portfolios, and many invest exclusively in mutual funds. This makes sense – mutual funds are easy to purchase, simple to understand, and they allow for continuous reinvestment of dividends and income earned by the mutual fund shares. As donors review their financial assets to determine which ones to use to fund charitable gift annuities, mutual funds present an obvious choice. As an added bonus: mutual funds are easy to value for gift purposes. The share price of a mutual fund is determined daily and published as the “Net Asset Value (NAV).” A donor uses this share price to value a gift of mutual fund shares. In contrast, a gift of publicly traded securities must be computed as the average of the high and low trading prices on the date of the gift.

But gift planners should be aware of some particular aspects of mutual funds that can cause significant complications in the process.

Thou Shalt Not Alter Thy Gift Annuity Agreements

-This question comes up from time to time: can the non-profit organization that is sponsoring charitable gift annuities modify its templates for the gift annuity agreements? Sometimes a person at the sponsoring charity wants to change portions of the agreements from an aesthetic standpoint – they want the language to be more flowing, or they have unique terminology they would like to be incorporated into the agreements. In other situations, there is concern about the technical aspects of the agreements – perhaps a consultant or some other outside advisor thinks the terms should be stated differently. Whatever interest there is – however well-intended – behind the idea of modifying the gift annuity agreement templates, our general recommendation is NO! – don’t do it – don’t even think about doing it! Let’s discuss some of the reasons why.

Indexing the Qualified Charitable Distribution Amount

-The index adjustment uses the average Chained Consumer Price Index for All Urban Consumers (C-CPI-U) for each calendar year with 2022 as the base year. The average for a calendar year is taken from 9/1 of the previous year through 8/31 of the current year. Indexing starts with 2024, so the first adjustment will include 9/1/2021 - 8/31/2023. A fair estimate is that there will be an inflation adjustment of 10% to 15% for that period. If that is correct, the limit on outright QCDs would be between $110,000 to $115,000 and the limit on QCDs to a CGA would be between $55,000 to $58,000 (rounded $57,500 to nearest $1,000).

QCD to Life Income Gifts (the “Legacy IRA”) Frequently Asked Questions

-What is the “Legacy IRA”? Under certain circumstances, a donor can make a one-time tax-free Qualified Charitable Distribution (QCD) from their IRA in exchange for a life income gift. This is a once in a lifetime election, subject to the limitations explained below.

Don’t Be Scared Off by CGA Regulations

-For any charity operating a gift annuity program, the question, “In what states do we need to register?” has likely come up (perhaps more than once). That may be closely followed by a declaration “we’re not registering in…” and the naming of one or more states accompanied by horror stories of the level of regulation they impose. Although complying with state gift annuity regulations does not top anyone’s “things I enjoy” list, the desire to avoid a certain state’s regulations can interfere with the success of your program.

Fortunately, a charity can issue in half of the states without being subject to any gift-annuity-specific registration, and if you tack on the 14 states that require only a notice of intent to issue, then the total grows to 39 states. The complexity really comes with the 11 more highly regulated states: Alabama, Arkansas, California, Florida, Hawaii, Maryland, New Jersey, New York, North Dakota, Tennessee, and Washington. While for some organizations their donor base is such that they want to be able to issue gift annuities in all states, for many it will make sense to weigh the cost (in time and dollars) of compliance with the benefit of expected gifts.

The question of where to register and issue should take into account the geographic reach of an organization and where it might have donors, but also the level of regulation in a given state as compared to the potential for gifts.